If you have a home loan or a loan against property, you might have wondered about it. If you feel your EMI is too high. You think that you are paying more than necessary. In fact, Many people do pay extra. Interest rates shift over time. New lenders come in with better rates. Still, people stay with old high-interest loans. Although you can switch to a new lender but we might think switching loans is too complicated.

The truth is it works out much easier than we imagine. The savings add up to a lot. Your property could be self-occupied or rented out. Maybe it serves business needs. A balance transfer at the right time reduces your EMIs, your interest costs and helps you to repay debt quick. We break it all down here in simple steps.

What Is a Home Loan / LAP Balance Transfer?

A balance transfer simply means shifting your current running loan from your current bank/NBFC to another lender. But why should you consider switching to another?

You can switch because a new lender can offer you a:

- a lower interest rate,

- a reduced EMI,

- a better tenure,

- or better service.

It’s like switching to a cheaper internet plan — your usage remains the same, but your cost goes down.

How Much Can You Actually Save?

Even a 1% drop in interest rate can save you lakhs of rupees, because these loans have long tenures and large amounts.

Example for a ₹5 lakh loan (Home Loan or LAP):

- Current Interest Rate: 11.5%

- New Interest Rate: 9.5%

- Remaining Tenure: 12 years

You could save up to 60,000 to 80,000 if you transfer your current loan to new lender.

Why Borrowers Must Pay Attention

Most borrowers end up paying high rates for years because:

- They took the loan during an emergency situation

- They accepted the first available offer

- They didn’t track market interest rate changes

- They were unaware balance transfer was possible

But interest rates have dropped significantly in recent years, and switching lenders can reduce EMIs by ₹3,000 to ₹10,000 per month.

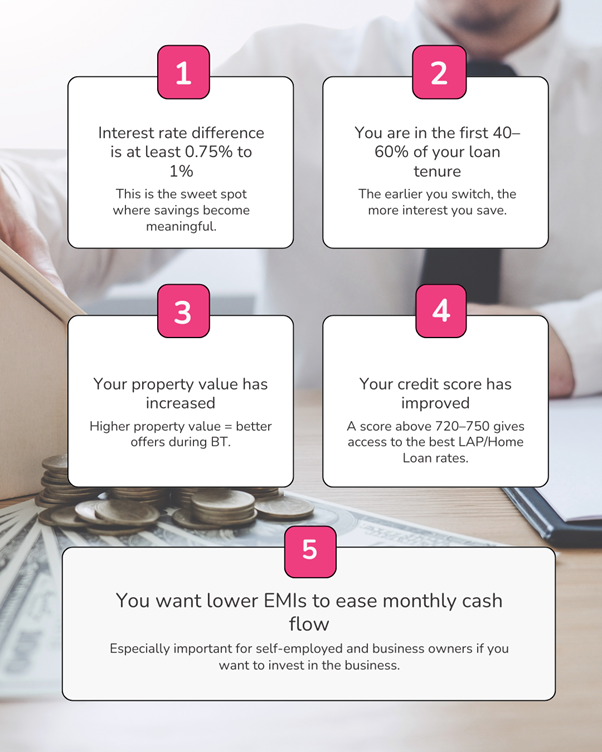

When Should You Consider a Balance Transfer?

You should evaluate switching if:

Documents Required for Home Loan / LAP Balance Transfer

Here’s the simple checklist:

- KYC documents (PAN, Aadhaar)

- Income proof (salary slips / ITR / bank statements)

- Existing loan statement

- Foreclosure letter

- Sanction letter

- Property papers

- Business financials (for self-employed)

The new lender usually coordinates 70–80% of the process directly with your existing lender.

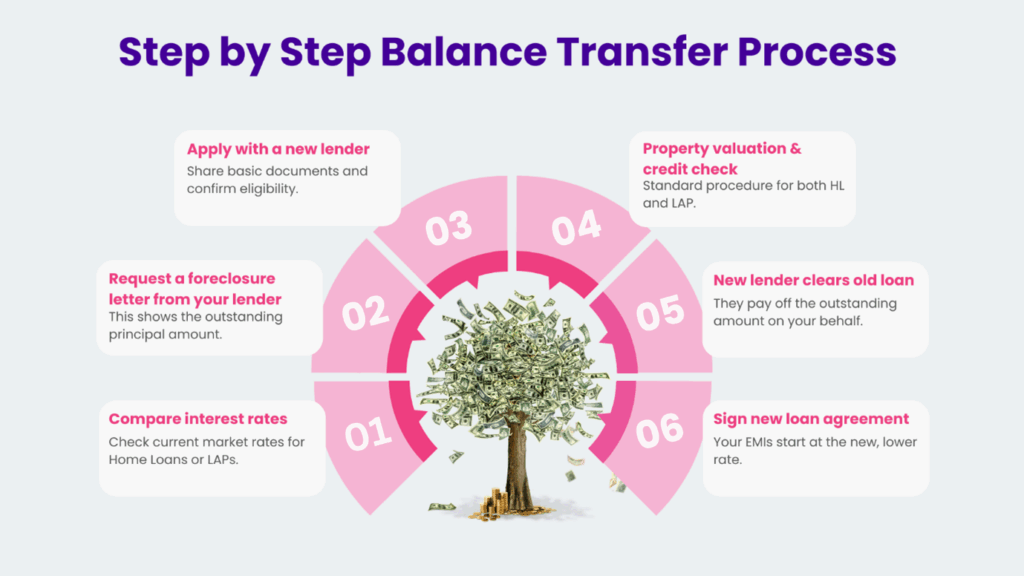

Step-by-Step Process to Transfer Your Loan Without Hassle

The moment you understand the process, the fear of “what if it’s too complicated” disappears. With the right lender and the right documents, transferring your Home Loan or LAP becomes a smooth, organised experience designed to save you money.

How Switching Lenders Helps Different Stakeholders

For Salaried Borrowers:

- Lower EMIs improve monthly savings

- Better repayment history boosts future loan eligibility

For Self-Employed / MSMEs:

- Lower interest = better cash flow

- Funds saved can be reinvested into business

- Higher value properties get better loan terms

For Families with Long Tenures Left:

- Even a 0.5% reduction generates huge lifetime savings

- Easier to manage household finances

Conclusion: Don’t Stay Stuck with a Costly Loan

If you took your loan years ago, your interest rate is probably outdated.

The lending market has changed. New lenders offer lower rates, flexible options, and faster processing.

A Home Loan or LAP Balance Transfer can help you:

- Reduce EMIs

- Save your hard-earned money

- Pay off your loan faster

- Improve financial security

- Unburden your monthly budget

There’s no reason to keep paying more when better options exist.